TL;DR: San Antonio’s real estate market in August 2025 displayed moderate activity with single-family home prices rising 5% year-over-year to $382,419 average, while inventory increased 15% and sales declined 7%, suggesting a shifting market dynamic favoring buyers.

Based on comprehensive data from the San Antonio Board of Realtors MLS for August 2025, the Alamo City’s real estate landscape presents a complex picture of adjustment and transition. While price appreciation continues across most segments, shifting inventory levels and sales volumes indicate a market finding its new equilibrium.

Single-Family Homes Lead Price Growth

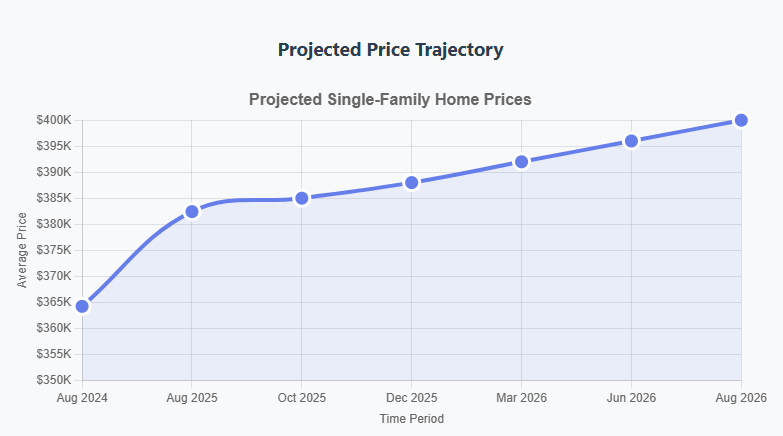

Single-family homes dominated market activity with 2,952 closed transactions in August, representing a 7% decline from the previous year. However, the average sales price reached $382,419, marking a solid 5% year-over-year increase. The median price of $310,000 grew 2% annually, demonstrating sustained demand despite reduced sales volume.

The existing home segment showed particular resilience, with average prices climbing 4% to $404,587. Buyers paid a median of $311,900, down 3% from last year, suggesting more affordable options entered the market. New construction averaged $344,396, up 5% year-over-year, though sales dropped 17% as builders adjusted to changing demand patterns.

Condominium and Townhome Sector Surges

Condominiums and townhomes experienced remarkable growth, with closed sales jumping 21% to 52 units. More striking was the 68% increase in dollar volume and 39% surge in average prices to $324,614. This segment’s median price of $211,500 rose 16% year-over-year, indicating strong demand for attached housing options.

The condo market’s performance suggests buyers are seeking more affordable alternatives to single-family homes, particularly as inventory in this sector increased 37% to 694 active listings.

Inventory Dynamics Signal Market Shift

Active listings across all property types painted a picture of increasing buyer choice. Single-family inventory climbed 15% to 17,043 homes, while pending sales decreased 17% to 2,459 transactions. This combination suggests buyers are becoming more selective, taking advantage of expanded options.

Days on market remained relatively stable at 74 days for single-family homes, up 12% from last year but still indicating reasonable market velocity. The price-to-list ratio of 91.4% shows sellers are adjusting expectations downward from previous peaks.

Rental Market Maintains Stability

Residential rental properties demonstrated remarkable consistency, with 1,509 closed transactions matching prior year levels exactly. Average rental rates of $1,877 remained flat, while median rents of $1,750 decreased 3% annually. This stability in the rental sector provides important housing options as affordability remains challenging for many residents.

Commercial and Specialty Sectors Show Volatility

Commercial properties declined 24% in transaction volume to 25 sales, though average prices surged 52% to $554,778. This pattern suggests fewer but higher-value commercial deals, possibly reflecting investor focus on premium properties.

Rural farms and ranches experienced significant activity with 46 sales, up 44% year-over-year. Dollar volume increased 42% despite average prices declining 1%, indicating strong demand for rural properties at various price points.

Year-to-Date Trends Confirm Market Moderation

Through August 2025, total single-family sales reached 22,996 transactions, down 3% from 2024. Despite reduced volume, dollar volume declined only 2% to $8.54 billion, with average prices rising 1% to $371,579. This data confirms the market’s gradual adjustment rather than dramatic correction.

Market Outlook and Implications

Looking ahead, several trends suggest continued market evolution. Rising inventory levels combined with stable pricing indicate a gradual shift toward buyer-favorable conditions. The rental market’s stability provides a pressure valve for those priced out of homeownership.

For buyers, increased inventory and longer marketing times suggest more negotiating power and selection.

For sellers, realistic pricing aligned with current market conditions becomes increasingly important as buyer selectivity grows.

For investors, the commercial sector’s higher average values and the strong rural property demand present opportunities, while the stable rental market offers consistent cash flow potential.

The San Antonio market appears to be achieving a healthier balance between supply and demand after years of rapid appreciation. While growth continues, the pace has moderated to more sustainable levels that benefit both buyers and sellers seeking realistic transactions in Texas’s second-largest city.